Introduction:

Digital health, i.e, the use of digital technologies to improve health outcomes that encompasses a wide range of products and services.These include mobile apps and wearables that help patients manage their own care; remote monitoring systems that allow clinicians to track patient data from afar; virtual reality tools for pain management and rehabilitation; artificial intelligence algorithms that analyze medical records for early detection of disease and readmission; telemedicine programs that provide remote consultation with doctors via video chat or phone call (and now even text message!).

With 2022 having a reasonable start amongst investments in digital health for the first half of 2022, a sharp decline persisted throughout the rest of the year. The deal flow and sizes equated to just over $15 billion dollars with over 575 deals throughout the entire year. Large investments declined for late stage companies by 60 percent and 33 percent for early stage investments compared to 2021.

Silicon Valley Bank’s recent report on digital health investments in 2022 revealed a marked decrease in software and artificial intelligence (AI) ventures that are transforming healthcare all across the board. According to the report, venture capital (VC) investments decreased in almost all sectors in healthcare and with Q4 of 2022 produced a sharp decline in new investments and more structured term sheets.

Market healthcare exits plummeted in the year 2022 with many plans being halted after a massive IPO craze during 2021 with healthtech and device companies. For healthtech companies, 2022 was not a great year for the performance of the stock market in the sector and investors are pushing for more M&A deals. Healthtech was on pace to break the 2021 deal amount for M&A but with slightly smaller deal sizes. With the acquisition of healthtech companies that picked up might mean consolidation of the sector but stronger companies in the near future. For device companies, 2021 was a big year in terms of IPO’s and M&A but when 2022 turned around many companies focused on cash flow and putting IPO’s and acquisitions on the back burner with vascular related exits equated to 3.

Active Investors and Current state of Digital Health:

The current state of digital health investments in 2022/23 is a reflection of the past few years. In 2016, there was an increase in investments due to an increase in funding rounds and valuation. In 2017, there was a decline in funding rounds but an increase in valuation. The same trend continued through 2018 with a decrease in funding rounds and another increase in valuation.

In 2022, we saw an even stronger focus on artificial intelligence (AI) as well as blockchain technology within the healthcare industry. AI will allow doctors to diagnose patients faster by using machine learning algorithms that analyze data from medical records or MRI scans; while blockchain technology will help protect patient privacy while also making it easier for patients to access their own information without having to go through their doctor first through applications and virtual care.

Some of the most active investors in the space for the year 2022 according to deals closed were:

- Gaingels – 24

- General Catalyst – 20

- Alumni Ventures Group- 15

- GV – 10

- Insight Partners – 9

- A16z – 5

The investment activity started to grow from 2022 – H1 2023, here we have a chart that discloses the growth from 2022 and Gaingels still looks like they are the most active in healthtech by deals closed:

Institutional investors have dry powder ready to be deployed but from an entrepreneur perspective, that also means that investors have raised the bar on what milestones founders need to achieve before they begin to invest.

Projections for Digital Health Investments for 2023:

According to the Rock Health 2023 Q1 digital health funding, there have only been 6 mega deals that have raised 9 figures for the quarter listed:

- Monogram Health ($375M)

- Shiftkey ($300M)

- Paradigm ($203M)

- ShiftMed ($200M)

- Gravie ($179M)

- Vytalize Health ($100M)

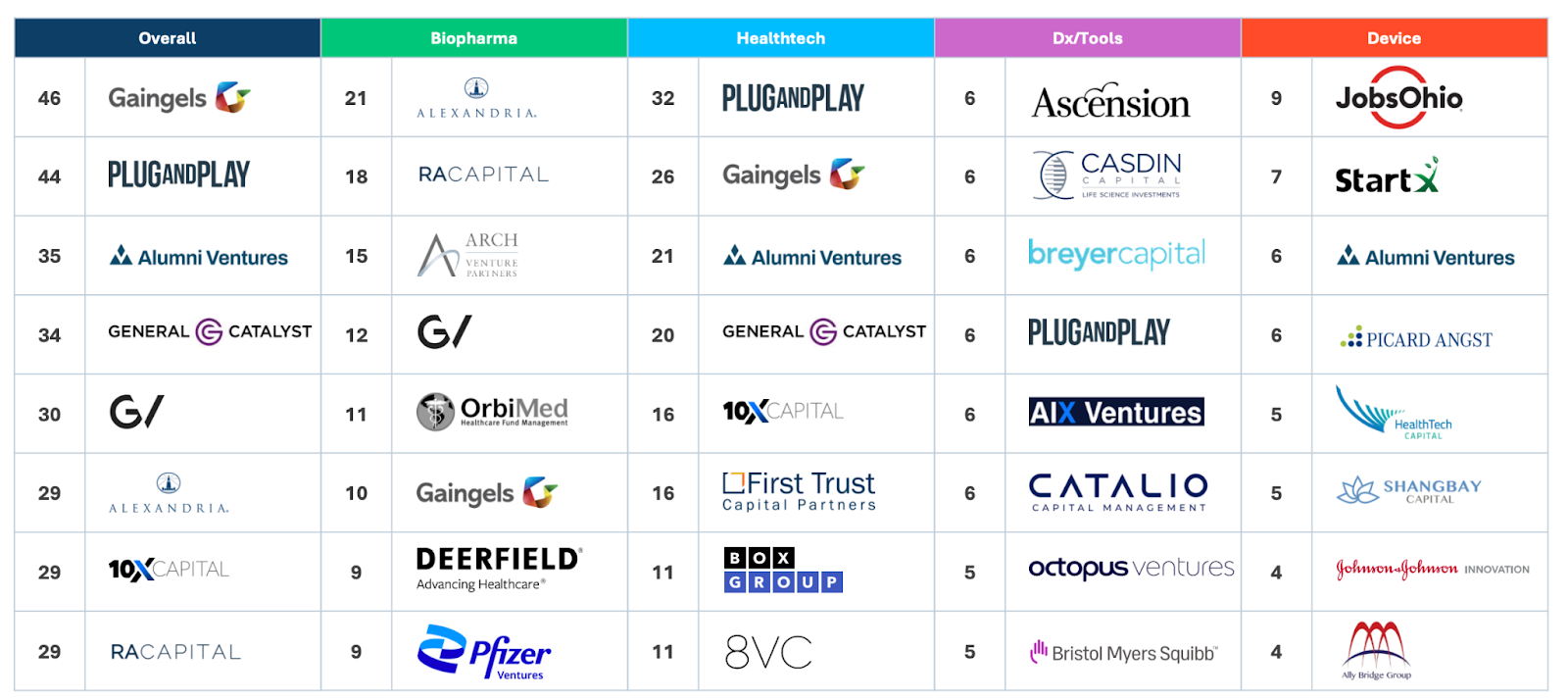

Accounting for 40 percent of the total digital health funding in the industry. With these very few deals being completed, it shows that investors are being even more selective over teams and founders they already know so they can use some of the reserves they have stockpiled in their funds. For example, Paradigm is one of the mega deals that were done where General Catalyst and ARCH venture partners co-incubated the company that came out with a $203M series A round. Here we show some of the most active institutional investors in the seed and series A rounds across all domains in healthcare. This includes investments made in the U.S, EU, and UK (Figure 1):

Figure 1 Chart provided by Silicon Valley Bank H1 report

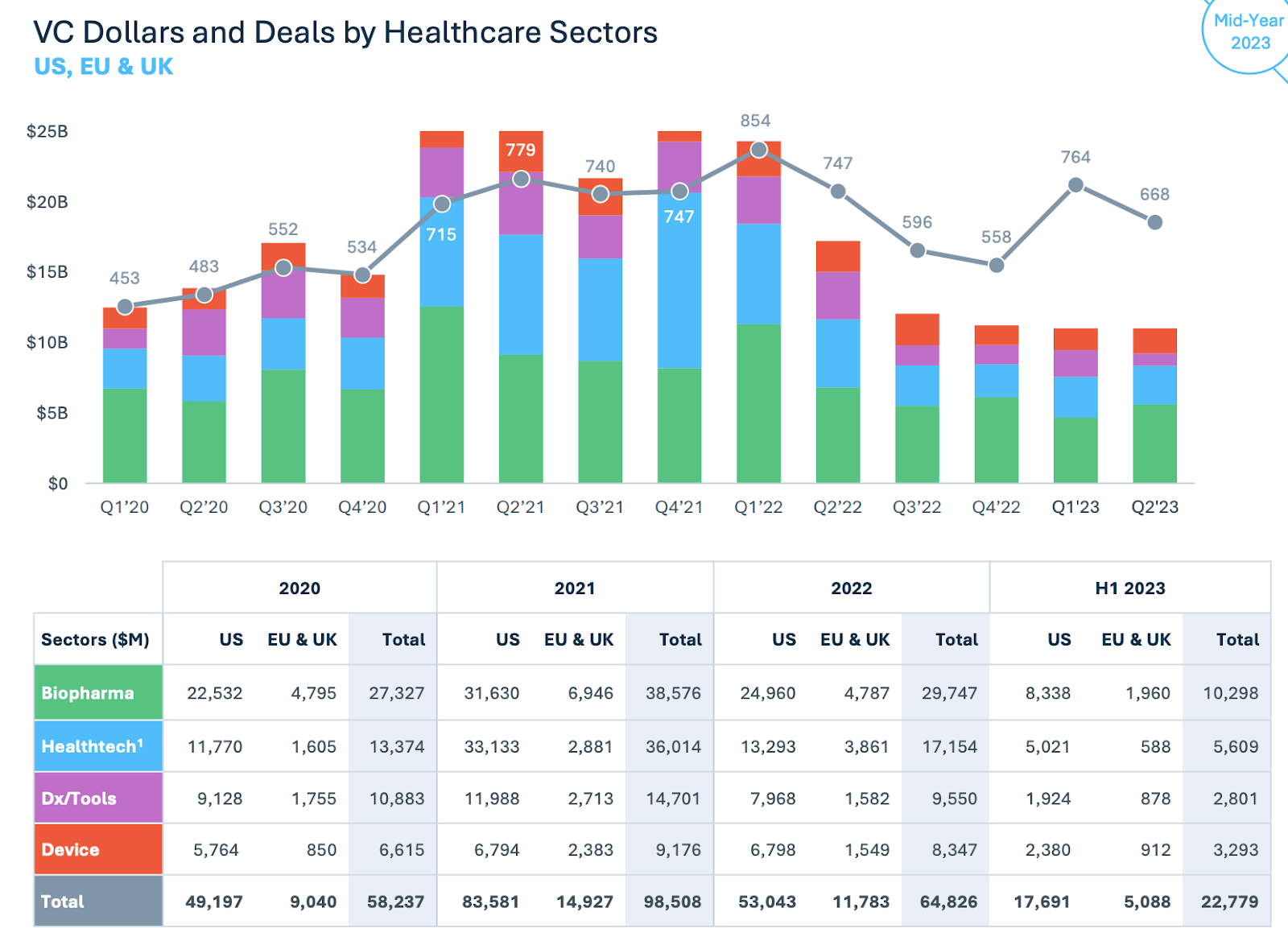

In Q’2 of 2023 we have seen an increase in funding amounts across verticals as seen in the chart below (Figure 2) that is parsed out by sector type:

Figure 2 Provided by Silicon Valley Bank

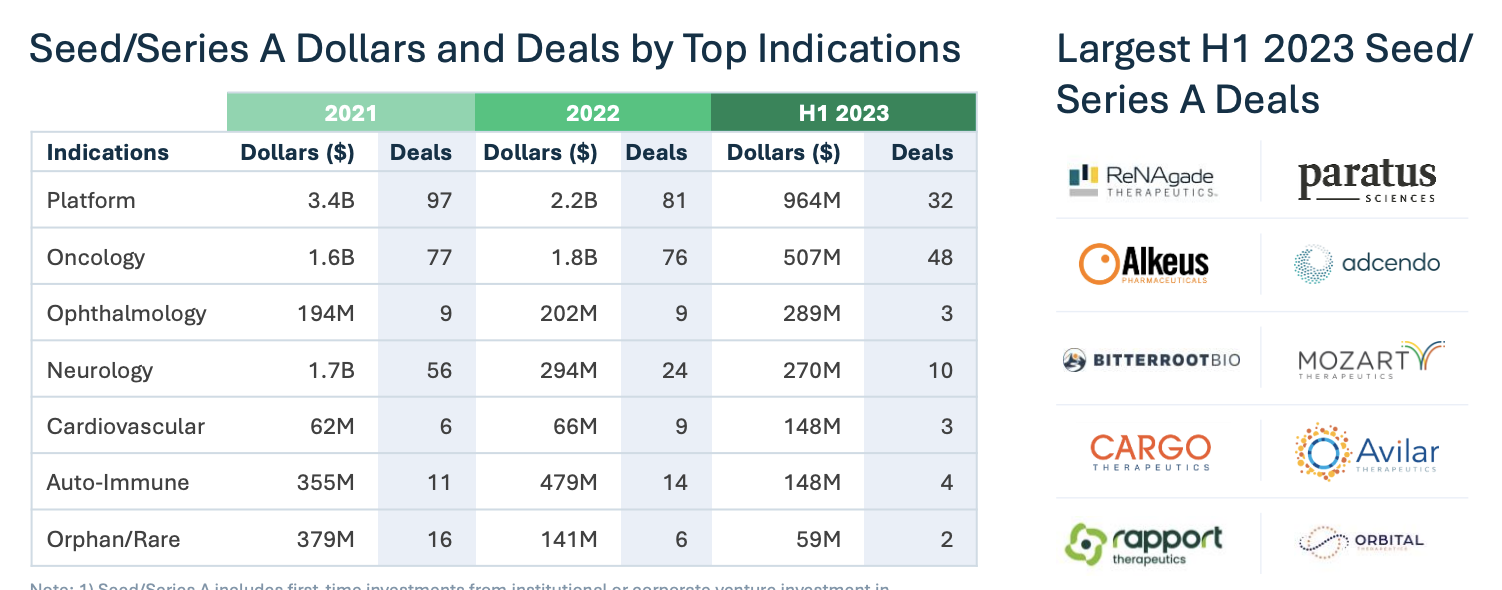

In total, around $6.8 billion dollars has been invested into healthcare which covers Biopharma, Healthtech, Dx/Tools, and Devices in Q ‘1 of 2023. So the amount of capital is down but also stabilizing a bit with a percentage change in those sectors ranging anywhere from 10 percent to 66 percent decline compared to Q ‘1 of 2021. The largest amount of dollars that are being allocated toward specific indications are oncology in terms of the numbers of deals (17) and platform indications with the largest amount of capital invested equating to $325 million to Q ‘1 of 2023.

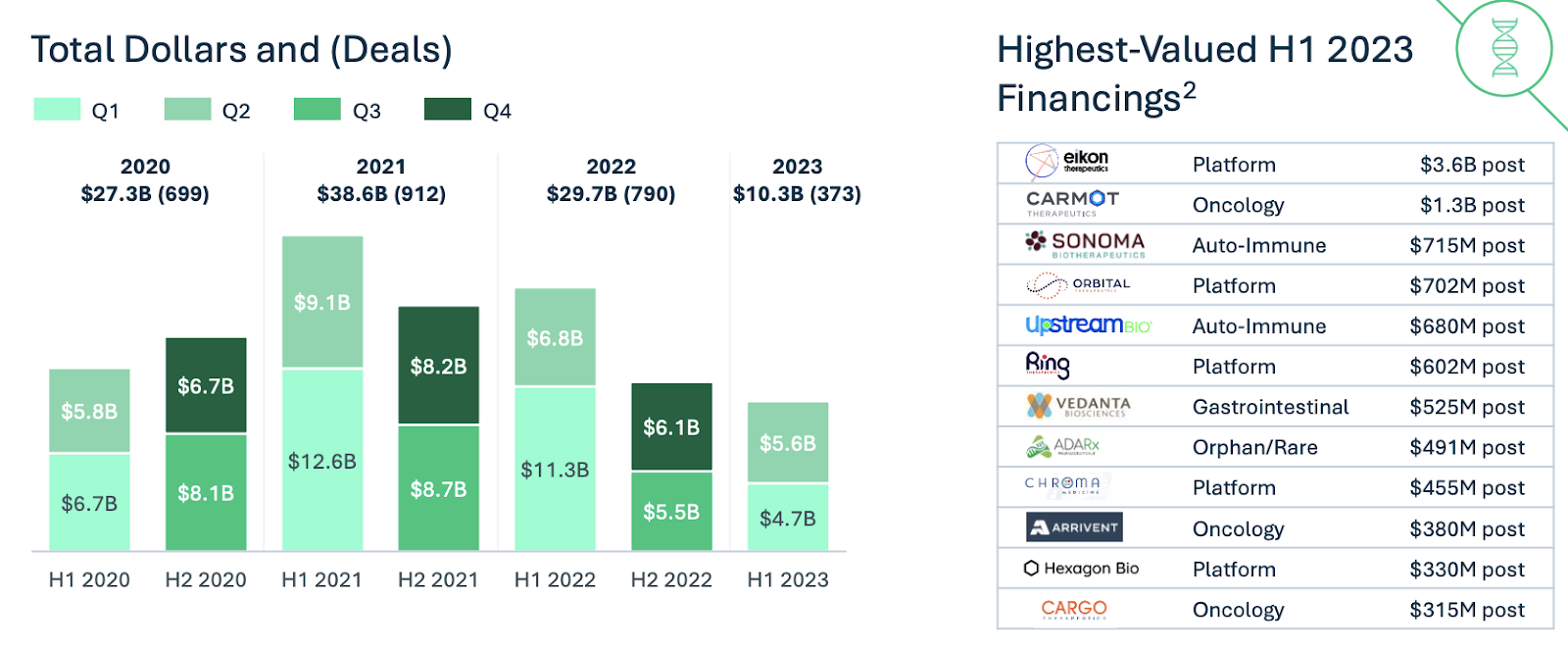

On the other hand, market economics has also played a large role in negative impacts on fundraising for digital health startups such as the collapse of Silicon Valley Bank, Signature Bank, and Silvergate Bank. Late stage companies had to seek assistance to be able to pay their staff and expenses which lead to seeking cash through alternative exit strategies like Public Benefit Corporation, debt financing, or liquidating assets within their business to stay afloat. While the digital health landscape seems unpredictable, there seems to be change coming on the horizon. However, late stage Biopharma companies seem like they have had a few winners in the raising capital space especially the platform based biopharma companies bringing in over $5.6B in Q’2 of 2023 as shown in Figure 3:

Figure 3 provided by Silicon Valley Bank H1 report

Some of the largest predictions have been that digital health investments will continue to stabilize throughout the year but at a decline compared to the year 2021. Some exports are saying that it may never get as high as the capital being allocated to companies in the year 2021. According to Silicon Valley Bank, they believe that the short term outlook is looking foggy but should have a strong finish during the 2nd half of the year. Some of the best companies in the world have grown to be the best and strongest companies coming out of uncertain times and I believe this year will be no different.

Impact of digital health investments:

Healthcare providers – Digital health investments are expected to provide a positive impact for the provider workflow both directly and indirectly. They can help providers streamline their processes through automation, intake more patients, provide better patient outcomes, and improve patient experience.

Payers- Chronic disease management is a large issue in the U.S. with the Center of Disease Control stating that 60 percent of Americans have a chronic condition. Digital health products can help build interventions between illnesses, nudges and patient education to help lower the cost of care. Care navigation is also a strong issue with only one out of ten Americans having the health literacy to be able to navigate the complex U.S. healthcare system. Services that can help offer patient hassle-free ways to manage their health plan, care coordination and utilization management will be beneficial in reducing costs.

In conclusion, we saw a strong start to digital health investments during 2021, first half of 2022 and a decline since then in both early, growth, and late stage investments. As the first half of the year came to a close we have seen an increase in funding but at lower valuations of companies. The markets look like they are making a strong turnaround for the 2nd half of the year across all sectors.

Citation:

- https://www.svb.com/globalassets/trendsandinsights/reports/healthcare/healthcare-investments-and-exits-annual-report-2022.pdf?utm_source=svb&utm_medium=pr&utm_campaign=gb-2023-01-aw-tl-ag-na-lh-na&utm_content=1pr_pct_oc_na_di_na_lp_auto&mkt_tok=NjEwLUtBSy0yNjYAAAGJbFxNdxBtkpmFbZYduDKTsNnFSvweS-RX4S3Xm1Vg9m-Y3ie3dgvL7Xfv2fBurPz_KJjz2SNDKDUmsFmc7Iso8V5Sn3kX16cZlH5kg7aEph5l

- https://rockhealth.com/insights/2023-q1-digital-health-funding-investing-like-its-2019/

- https://www.fdic.gov/bank/historical/bank/bfb2023.html

- https://www.healthleadersmedia.com/finance/cas-safety-nets-lost-32b-first-18-months-pandemic

- https://www2.deloitte.com/us/en/insights/industry/health-care/digital-health-plan.html

- https://www.svb.com/globalassets/trendsandinsights/reports/healthcare/2023/healthcare-investments-and-exits-annual-report-q1-2023.pdf

- https://www.svb.com/globalassets/trendsandinsights/reports/healthcare/2023/mid-year/healthcare-investments-and-exits-mid-year-2023.pdf